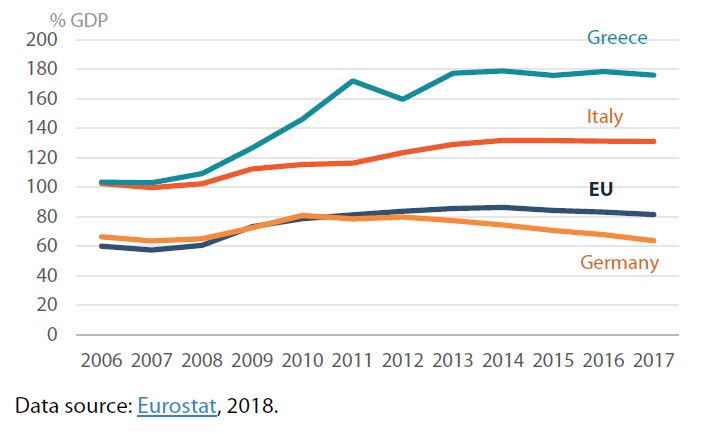

In hindsight, the EU took extraordinary measures to prevent a repetition of an even greater crisis than that of the 1930s. Three main kinds of action were deployed: at EU level, central bank level and government level. In 2008 a large stimulus package called the European economic recovery plan (EERP) was launched by the EU. The ECB took measures to support banking sector liquidity and accommodate the funding needs of banks. The governments also supported the financial system by increasing deposit insurance ceilings, providing guarantees for bank liabilities, and recapitalising banks being bailed out or wound down. In addition, they implemented fiscal measures to reduce the fall-out of crisis on the rest of the economy. This resulted in a mix of ‘automatic stabilisers’ (decreasing tax receipts coupled with increased government welfare payments as the economy slows down) and targeted discretionary fiscal measures, such as additional public investment, tax relief and subsidies for part-time employment. These actions led to a dramatic escalation of public debt (Figure 2).

Be the first to write a comment.