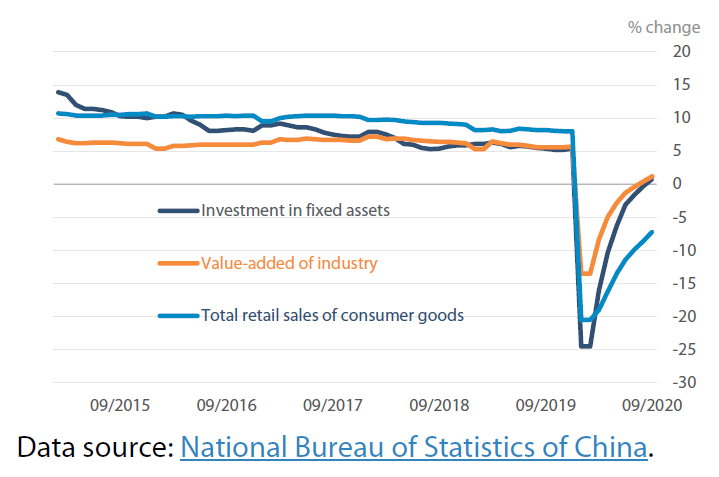

China’s rapid economic recovery provides evidence of strength, but there are structural weaknesses. While supply-side constraints have eased, weak domestic and external demand have restrained the pace of recovery, despite the wide range of measures taken to mitigate the economic fallout.

In September 2020, overall industrial output increased by 6.9 %, contrasting sharply with a modest 1.2 % growth year on year during the first three quarters. It is noteworthy that high tech manufacturing and equipment manufacturing have proved very resilient. Their figures soared by 5.9 % and 4.7 % respectively year on year during the first nine months of 2020.

The industrial products with the biggest output growth rates – trucks (23.4 %) and excavators and shovelling machinery (20.2 %), a barometer for infrastructure construction activity – industrial robots (18.2 %), and integrated circuits (14.7 %) suggest a dual-track trajectory of the recovery combining traditional state-backed infrastructure construction with market-driven demand for equipment for the digital economy. Lockdown-induced demand for home office equipment for instance has sustained a constant rise in micro computer equipment output of over 5 %.

Be the first to write a comment.